Disability insurance has always been the red-headed stepchild, the black sheep, the misfit of the insurance world. It's a much harder sale than it's golden child counterpart, life insurance. However, statics show that an individual has a 1 and 4 chance of becoming disabled during the working years. The top five causes behind long term disability claims are not radical or uncommon, so why are 51 million working adults in American without disability insurance? One of the main challenges with disability insurance is how it is marketed.

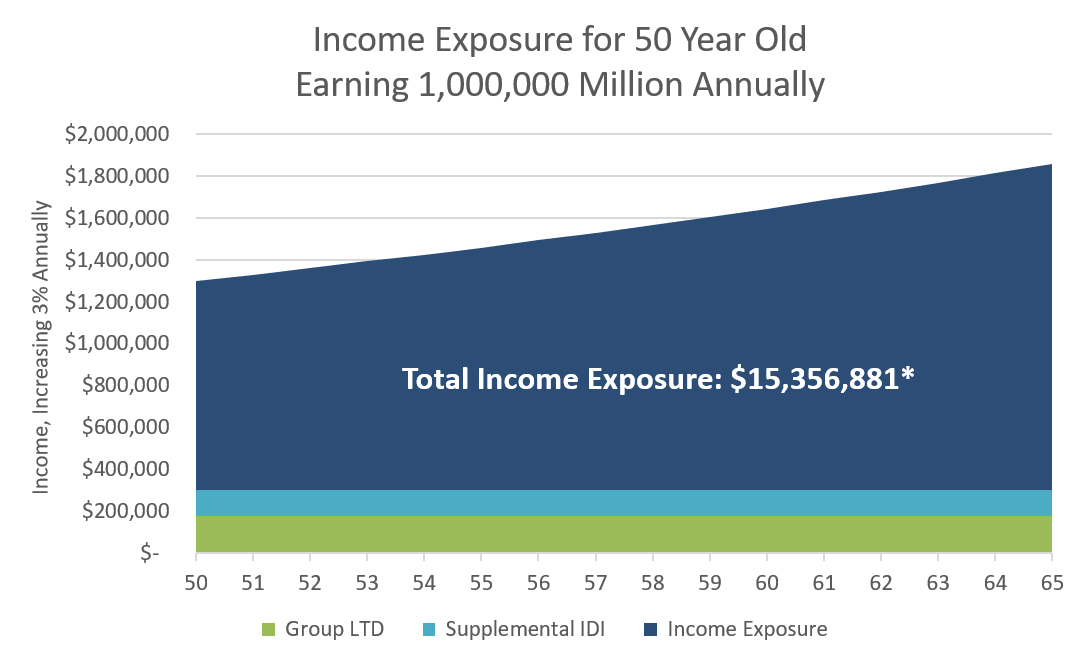

When you are out of work due to a stroke, cancer, or a degenerating disk, you are losing your ability to earn an income - the biggest asset you have. On a grand scale, take a 50-year-old executive earning seven figures annually with a time horizon of 15 years until retirement. This executive has over a $15 million exposure to their estate in the event he or she were to suffer an injury, or more likely, a serious illness.

What do you own that is worth $15,000,000 that is not insured or severely underinsured? Most likely, nothing!

Thanks to the powerful resources offered via Lloyd's of London, high earning individuals can access extraordinary benefit limits to supplement the programs they have purchased in the U.S., or secure coverage where options did not exist.

Once we wrap our heads around that disability insurance = income protection, the conversation shifts. Income protection implies that you are in control of your future and have laid out a plan to protect your estate and family.

BONUS: Download a collection of our best case studies

*Assuming $25,000/mo in domestic disability coverage and an annual income increase of 3%.