The term “American Dream” was originally coined by James Truslow Adams in his book, The Epic of America. Since the first publication of the book in 1931, the term has since been used by American society to conjure images of job success and the classic American material possessions: the three-bedroom house, the white-picket fence with two and a half kids and a Labrador. However, for those earning an income in the top ¼ of the top 1%, the American Dream transforms into an entirely different lifestyle: a seven-figure income, a 6-bedroom house, kids in private school, luxury cars, and of course, a vacation home in a choice location. Unfortunately, these are the individuals with the largest gap in disability insurance protection.

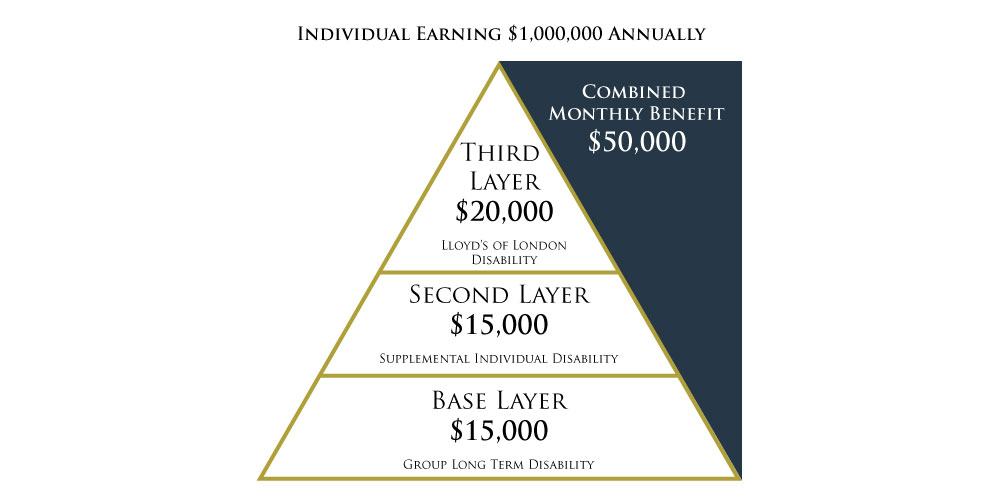

For your highly compensated executive clients who have the grit and tenacity to develop a seven-figure income, they often find themselves with an exposure to their future estate exceeding 15 million. To exemplify, take a 40-year-old individual earning a million dollars with a time horizon of 15 years (minimum!) until retirement, a $15 million exposure to their estate exists in the event they suffer an accident or illness rendering them unable to work. For these ultra successful clients, implementing a sound income protection strategy should be the foundation of their financial plan when protecting their family's future wealth. Not only does proper planning protect their 1% lifestyle, but it also protects a multi-million-dollar fortune.

Download Case Study of High Level Executive

As an advisor, minding the gap in your executive's disability insurance plan is crucial. When the US disability insurance markets cannot provide a sufficient amount of coverage your client is looking to purchase, one can access the power and resources of the Excess Lines Market to enhance a domestic disability plan. High limit disability income protection is most often utilized to supplement an individual’s US disability insurance coverage to provide adequate protection for high income earners.

This type of coverage typically provides an “own occupation” definition of disability. Own occupation means that by purchasing a supplement plan with true own occupation coverage, you have the ability to earn additional income in another profession while disabled under the occupation you sought coverage to insure.

If you are interested in discovering how to unlock DI opportunities in this space, we will be hosting a webinar on May 26th. Please register here.